Discount is an allowance provided to the customers in specific circumstances. In business, there are two main types of discounts, i.e. trade discounts and cash discounts. While trade discount is the reduction in the list price of the product, whereas cash discount is offered by the firms to its customers to encourage early payments.

Discount is an allowance provided to the customers in specific circumstances. In business, there are two main types of discounts, i.e. trade discounts and cash discounts. While trade discount is the reduction in the list price of the product, whereas cash discount is offered by the firms to its customers to encourage early payments.

The main difference between trade discount and cash discount is that a separate ledger account for discounts allowed is opened in the books of the seller and discount received in the books of the buyer for a cash discount, but no such account is created in case of a trade discount.

What is a Discount?

The term ‘discount’ refers to the deduction at a specified rate from the total amount receivable or payable based on the terms of the agreement. Therefore, if the discount is allowed, the receiver receives a lesser amount than the amount due, and the payer pays less amount than what is actually due to him. Hence, it is a loss to the one receiving payment but a gain to the person paying it.

Also Read: Difference Between Discount and Rebate

In this written material, we have discussed the differences between trade discount and cash discount.

Content: Trade Discount Vs Cash Discount

- Comparison Chart

- Definition

- Key Differences

- Example with Journal Entry

- Points to Remember

- Conclusion

Comparison Chart

| Basis for Comparison | Trade Discount | Cash Discount |

|---|---|---|

| Meaning | Trade Discount refers to the deduction given by the supplier to the customer in the catalog price of the goods. | Cash discount implies the allowance granted to the customers by the supplier on the invoice price, for immediate payment. |

| Basis | Based on the amount of purchase or sales | Based on time, i.e. Period of payment |

| Fixed Percentage | Yes | May or May not be fixed |

| Why Allowed? | Because of business considerations like trade practices, orders in bulk, etc | As an incentive or motivation, for payment within a specified time. |

| Objective | To increase sales in bulk quantity. | To encourage early and prompt payment. |

| Allowed on | Both Cash and Credit Transactions. | Only on cash payments. |

| Entry | Not entered in the books of accounts. | Appears as an expense in Income Statement. |

| Deduction | Deducted from the invoice value or catalog price of the goods. | Deducted from the invoice value of goods. |

Definition of Trade Discount

Trade Discount is the discount which the manufacturers or the wholesalers offer to their customers, on a fixed percentage basis on the catalog price of the goods, at the time of sale. It is used as a tool by the manufacturers to attract customers, increase sales volume, and encourage bulk purchases. Therefore, with the increase in the volume of purchases, the rate of discount also increases in general.

- The important aspect of trade discount is that it is neither debited nor credited in the journal entry. Therefore, the amount of discount is reduced from the listed price and the journal entry in relation to purchases is made with the reduced price.

- Moreover, at the time of purchase or sales return, trade discount is once again reduced from the catalog price of the goods, and entry of the net amount is made.

Once the discount is charged, the net amount which the customer has to pay is determined. And this net amount (net sales price) is recorded in the books of account. Further, a trade discount is offered in case of both cash sales and credit sales. So, when there are cash sales, it is deducted from the cash memo, whereas in the case of credit sales, the amount of discount is deducted from the sales invoice.

Example

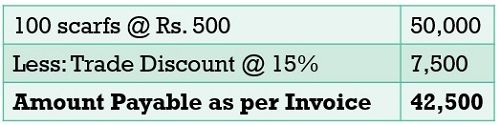

Suzan bought 100 scarfs, from Kim for Rs. 500 each, subject to Trade Discount @ 15%. So, the net amount payable by Suzan is:

What is List Price?

List Price is the proposed retail price, which the manufacturer or distributor decides, and is listed in their catalog. The difference between the list price and the amount of discount is the net price.

Also Read: Difference Between Invoice and Cash Memo

Definition of Cash Discount

Cash Discount is a concession provided to the customers at a specified rate, for satisfying certain conditions of payment, primarily related to prompt cash settlement and also to avoid the credit risk. As the name suggests, cash discount is associated with cash flow, i.e. cash receipt or cash payment.

It encourages the buyer of the goods to make payment at the earliest in order to avail cash discount, and so he will have to pay a lesser sum, than the sum actually due to him. It is provided when the purchaser makes timely or early payment for the goods bought.

- Cash Discount recorded at the debit side of the cash book as discount allowed, whereas discount received appears at the credit side of the cash book.

- Such discount is allowed only when the customer makes payment of the debt within the stipulated time, i.e. prior to the expiry of the credit period.

- It is calculated on a percentage basis on the total amount payable by the customer.

Example

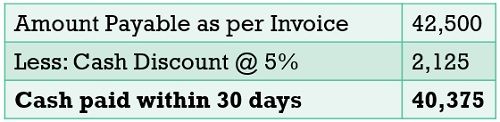

Suzan bought 100 scarfs, from Kim for Rs. 500 each, subject to Trade Discount @ 15%. Further, if the terms of payment are 5%, 30 days. This means that an additional 5% cash discount will be allowed to Suzan if she makes payment within 30 days.

Also Read: Difference Between Voucher and Invoice

Key Differences Between Trade Discount and Cash Discount

As we have discussed the meaning and example of the two types of discount, now we will move forward to talk about the differences between trade discount and cash discount:

- Trade Discount is a subtraction from the list price of the goods, allowed by the trader to the customer at an agreed rate. On the contrary, a Cash Discount is a discount allowed to the customer, when he/she makes cash payment of the goods purchased, within the stipulated time.

- Trade discount is based on the amount of purchase or sales, i.e. the more the sales the more will be the rate of discount, whereas cash discount is based on time, i.e. the earlier the payment made by the debtor, the more will be the cash discount allowed.

- Trade Discount is always provided to the customer in fixed percentage, whereas the percentage of cash discount may or may not be fixed.

- Trade Discount is allowed to the customers because of business considerations like trade practices, bulk orders, etc. Conversely, Cash Discount acts as an incentive or motivation for stimulating payment within the specified time.

- Trade Discount is provided to increase sales in bulk quantity, while Cash Discount is given to the customers to encourage early and prompt payment.

- Trade discount is allowed on both cash and credit transactions. In contrast, a cash discount is allowed to the customers only on cash payments.

- Trade Discount is not specifically shown in the company’s financial books, and all the transactions are entered in the purchases or sales book in net amount only. In contrast, Cash Discount separately appears in the financial books, as an expense in the Profit and Loss Account.

- Trade Discount is deducted from the invoice value or catalog price of the goods. As against, Cash Discount is deducted from the invoice value of goods

Example with Journal Entry

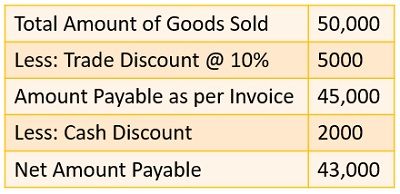

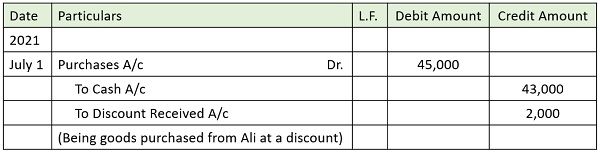

Suppose James purchased goods from Ali of the list price of Rs. 50,000, on July 1, 2021. Ali allowed a 10% discount to James on the list price, for purchasing goods in bulk quantity. Further, a discount of Rs. 2000 was allowed to him, for making the payment within 30 days.

So, first of all, the discount allowed on the list price of the goods, i.e. 10% of Rs. 50000 = Rs. 5000, is a trade discount, which is not going to be recorded in the books of accounts.

Next, the discount received by James of Rs. 2000 for making the quick payment is a cash discount, as it is allowed on the invoice price of the goods. A cash discount is entered in the books of accounts. Therefore, the journal entry for the transactions in the books of James is:

Journal Entry

Points to Remember

- In case when both the discounts are allowed to the customer, in a transaction, then the trade discount is allowed on the list price first, then cash discount is allowed on the net amount payable.

- Discount is a Nominal Account, so the discount allowed is an expense for the company so it is an expense account, whereas the discount received is a gain for the company so it is a revenue account.

Conclusion

Basically, trade discounts are the discounts allowed by the manufacturers or wholesalers to the customers with an aim of increasing the sales volume, whereas cash discount is allowed to the customers by the sellers to increase the cash flow. A customer can enjoy both trade discounts and cash discounts if he/she is making cash payments for the goods purchased.

T M Maung says

Short and sweet.

Vinit says

Very good site. I have got exact & valuable information of accounts here. Thank you so much.

Francis says

Thanks for this! Short yet really understandable

Subhan says

Amazing way of clearing the concept..Thankx

Jaocb says

Great,

clear and precise information.Thanks a million

Aariz says

Great,

Nice and clear.

Thanks a ‘MILLION’

QuickBooks help says

invoice is correct or not. When you would confirm about invoice then you can send an invoice for customers with a payment link and check payment is received or not

Poni says

Perfect, clear and simply explained easy to understand, thanks ‘BIG’